How Much Downpayment Do You Need for a Home Loan? Your Ultimate Guide (2026)

Buying a home is a big leap—and in Singapore’s fast-paced, competitive property market, it all starts with nailing down your downpayment. Whether it’s an HDB flat, a shiny BTO unit, or a luxurious condo, the question looms large: How much do you need upfront? The answer hinges on the property type, your loan, and even your citizenship status. With prices climbing and rules tightening, planning your upfront cost isn’t just smart—it’s your ticket to staying ahead in this race. Let’s break it down with practical examples, tips, and everything you need to know in 2025. Ready? Let’s get started!

Table of Contents

ToggleWhat’s a Downpayment, and Why Does It Matter?

A downpayment is your upfront stake in a property’s purchase price, with the rest covered by a home loan. Think of it as your financial foot in the door. A larger initial contribution—whether for an HDB flat or a condo—can shrink your loan, cut interest costs, and lighten your monthly repayments. But it’s not a one-size-fits-all number. It varies by property type, loan terms, and your personal situation. So, what shapes this all-important figure? Let’s explore the key factors next.

What Determines Your Home Loan Downpayment?

Your upfront cost isn’t arbitrary—it’s calculated based on key factors banks and financial institutions, like those overseen by the Monetary Authority of Singapore (MAS), consider when approving your loan. Here’s what shapes it:

1. Your Citizenship Status Matters

Are you a Singapore Citizen, Permanent Resident (PR), or Foreigner (FR)? Your status directly impacts your upfront costs due to Additional Buyer Stamp Duty (ABSD):

Singapore Citizens get the most favorable terms with zero ABSD for their first property purchase.

Permanent Residents will incur a 5% ABSD levied on their first property purchase.

Foreigners will incur a substantial 60% ABSD levied on their first property purchase.

2. Loan-to-Value (LTV) Limits: The Key to Your Downpayment

The LTV ratio sets how much of your property’s value a bank will finance. Here’s the 2025 breakdown from MAS:

Housing Loan Requirements by Outstanding Loans

| Outstanding Housing Loans | Maximum LTV | Minimum Cash Downpayment |

|---|---|---|

| None |

Structure 1: 75% - Tenure till age 65

Tenure cannot exceed 30 years (Private Property) or 25 years (HDB) Or

Structure 2: 55% - Tenure till age 75

Tenure cannot exceed 35 years (Private Property) or 30 years (HDB) |

Structure 1: 5%

Structure 2: 10%

|

| One |

Structure 1: 45% - Tenure till age 65

Tenure cannot exceed 30 years (Private Property) or 25 years (HDB) Or

Structure 2: 25% - Tenure till age 75

Tenure cannot exceed 35 years (Private Property) or 30 years (HDB) |

25% |

| Two or more |

Structure 1: 35% - Tenure till age 65

Tenure cannot exceed 30 years (Private Property) or 25 years (HDB) Or

Structure 2: 15% - Tenure till age 75

Tenure cannot exceed 35 years (Private Property) or 30 years (HDB) |

25% |

For example, with a 75% LTV, you cover 25% upfront—5% in cash, the rest potentially from your CPF Ordinary Account (OA).

With these factors in mind, let’s see how they play out across Singapore’s housing options—starting with the most popular: public housing like HDB flats and BTO units.

Public Housing Downpayments: HDB and BTO

For many Singaporeans, homeownership begins with public housing—HDB flats for immediate needs or Build-to-Order (BTO) units for a fresh start. The good news? These options are designed to be affordable, with flexible payment rules and grants to lighten the load. Here’s how it works in 2025.

HDB Downpayment: Your Affordable Entry

HDB flats are the backbone of Singapore housing, and their downpayment reflects that accessibility:

HDB Loan: A 25% downpayment of the purchase price is required, payable with cash, CPF, or a combination of both.

Bank Loan: A 25% downpayment of the purchase price is required, payable with cash, CPF, or a combination of both.

Example: A $500,000 HDB flat:

HDB Loan: $125,000 HDB (CPF or cash).

Bank Loan: $125,000 ($25,000 cash + $100,000 CPF/cash).

Citizen Perks:

BTO Downpayment: Fresh Flats, Flexible Payments

A Build-to-Order (BTO) flat offers a brand-new start, and the BTO downpayment is tailored for young buyers. For flats from the June 2024 sales exercise onwards, HDB introduced a phased structure, per HDB:

- HDB Loan: The downpayment is 20%, split as 2.5% in cash or CPF OA when signing the Agreement for Lease, and 17.5% in cash or CPF OA at key collection.

- Bank Loan (75% LTV): Total downpayment is 25%, with 2.5% in cash only at signing, and 22.5% (including 2.5% cash minimum) in cash or CPF OA at key collection.

- Bank Loan (55% LTV): Total downpayment is 45%, with 2.5% in cash only at signing, and 42.5% (including 7.5% cash minimum) in cash or CPF OA at key collection.

Example: A $350,000 BTO flat:

- HDB Loan: $70,000 downpayment total ($8,750 at signing [cash/CPF], $61,250 at key collection [cash/CPF]).

- Bank Loan (75% LTV): $87,500 downpayment total ($8,750 cash at signing, $78,750 at key collection [$8,750 cash minimum + $70,000 CPF/cash]).

Grants can offset this, and the phased downpayment spreads the cost. PRs add 5% ABSD ($17,500 extra). Note: Bank loans require at least 5% cash (75% LTV) or 10% cash (55% LTV) of the purchase price before disbursement, per HDB rules.

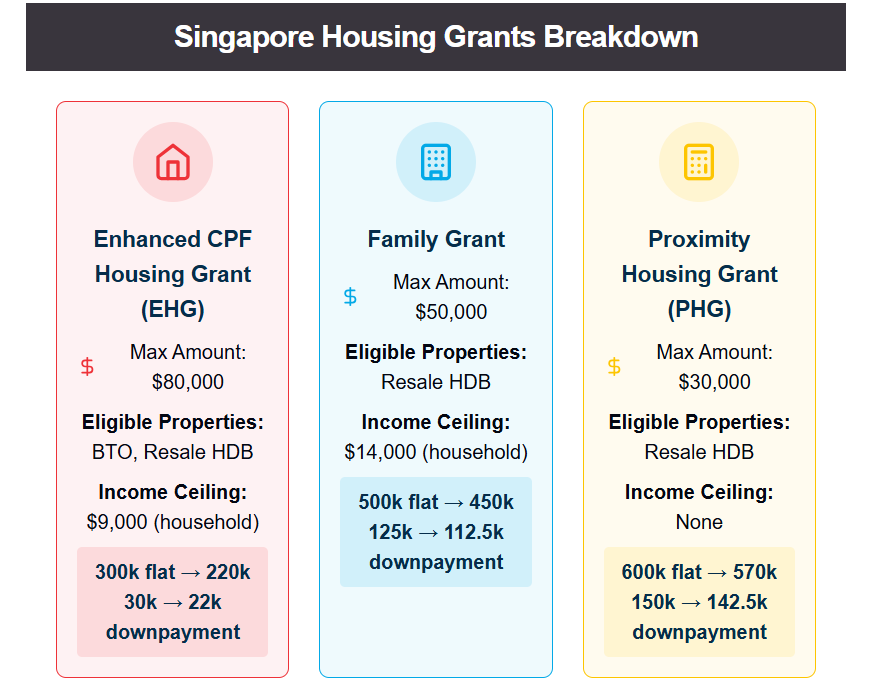

Grants: Your Financial Lifeline

Singapore offers grants that directly reduce your upfront costs for HDB/BTO purchases. Here’s a quick guide to the key 2025 grants:

Housing Grants Comparison

| Grant Name | Max Amount | Eligible Properties | Income Ceiling (Monthly) | Downpayment Impact Example |

|---|---|---|---|---|

| Enhanced CPF Housing Grant (EHG) | $80,000 | BTO, Resale HDB | $9,000 (household) | Reduces a 300k flat to 220k → Downpayment drops from 30k to 22k (HDB loan) |

| Family Grant | $50,000 | Resale HDB | $14,000 (household) | Reduces a 500k flat to 450k → Downpayment drops from 125k to 112.5k (bank loan) |

| Proximity Housing Grant (PHG) | $30,000 | Resale HDB | None | Reduces a 600k flat to 570k → Downpayment drops from 150k to 142.5k (bank loan) |

How It Works: Grants go to your CPF OA, directly cutting your initial outlay. Check eligibility on the HDB website—first-timers get the biggest boost.

So, public housing keeps things budget-friendly. But what if you’re eyeing a private property upgrade? Let’s shift gears to condos.

Downpayment for Condos: The Private Property Leap

Dreaming of a condo with a pool and gym? The downpayment for a condo—or condominium downpayment—steps up the game, governed by MAS bank loan rules—no HDB loans here:

Minimum Requirement: The downpayment for a condo is 25%, with 5% in cash and 20% from CPF or cash.

LTV Limits: Up to 75% for your first property, dropping to 45% or 35% for additional homes, raising the downpayment for a condo.

Example: A $1.5 million condo:

Total = $375,000 ($75,000 cash + $300,000 CPF/cash).

HDB vs. BTO vs. Condo: A Quick Glance

Not sure which fits? Here's a comparison:

| Property Type | HDB Loan Downpayment | Bank Loan Downpayment |

|---|---|---|

| HDB | 25% (Cash / CPF) | 25% (5% cash + 20% CPF/cash) |

| BTO | 25% (Cash / CPF) If Staggered: - 2.5% during signing of agreement - 22.5% during key collection |

25% (5% cash + 20% CPF/cash) |

| Condo | N/A (bank loan only) | 25% (5% cash + 20% CPF/cash) |

Beyond the Downpayment: Extra Costs

Your downpayment isn’t the full story. You’ll also face these additional costs when buying a property in Singapore:

- Buyer’s Stamp Duty (BSD): A mandatory tax on all property purchases. The amount varies based on the property price.

- Additional Buyer’s Stamp Duty (ABSD): PRs pay 5%, while foreigners face a steep 60%, significantly increasing upfront costs.

Buyer Profile ABSD Rate Singapore Citizens (1st) 0% Singapore Citizens (2nd) 20% Permanent Residents (1st) 5% Permanent Residents (2nd) 30% Foreigners(Any) 60% - Legal Fees by Cash/CPF (for a property purchase):

Private Property: $2500 +/-

HDB Resale: $1800 +/-

BTO: $2000 +/-Valuation Fees by Cash:

Private Properties: Depending on valuation, could range from a few hundreds to thousands

HDB: $120 nett

Use our free Stamp Duty Calculator to find your exact Buyer's Stamp Duty (BSD) and Additional Buyer's Stamp Duty (ABSD) based on your citizenship, property type, and purchase price.

Smart Strategies for Managing Your Home Loan Downpayment

Ready to tackle your downpayment? Here’s how to stay ahead:

Clear existing loans if necessary: Loans reflected in your Credit Bureau Statement will impact your TDSR, minimizing these loans will help improve your borrowing power. Though the LTV will ultimately be capped at the purchase price or valuation, whichever is lower.

Check bank valuations before committing to a purchase: For resale private properties, we can help to get indicative valuations from various banks that will be useful for price negotiations. These valuations will prevent you from paying unnecessary Cash-Over-Valuation (COV). For resale HDB however, valuations are determined by HDB directly and you can only request for a valuation after paying the $1,000 Option Fee to the seller. The best you can possibly do is to check recent resale transactions that were completed in the same block for similar units.

Leverage on CPF: Monies in our CPF Ordinary Account can be used towards our property down-payments and mortgage instalments. This can be an alternate source of funding if there is a lack of cash liquidity.

Plan for BSD & ABSD: When purchasing a resale private property, both Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD) must be paid in cash to IRAS within 14 days of exercising the Option to Purchase (OTP). In contrast, for HDB flats and new launch private properties, stamp duties can be paid using cash or CPF funds. Make sure to account for this potential cash outlay in your overall financial planning.

Choose loan tenure wisely: Depending on how much loan you require, extending your loan tenure to age 75 could be a viable option.

Example:

Mr. Tan is 50 years old with a monthly salary of $6,000. He’s looking to purchase a $1 million property and wants the highest loan amount possible. He has no existing debts.His loan eligibility:

$446k over 15 years, capped at 75% LTV. Min 5% cash downpayment.

– If he chooses this option, his LTV will be 44.6% ($446k)Or

$625k over 25 years, capped at 55% LTV. Min 10% cash downpayment.

– If he chooses this option, his LTV will be 55% (550k)Hence, if he chooses to extend his loan tenure to 25 years, he could potentially get a higher home loan of $550k. Reducing his overall downpayment.

Explore Tools: Try our Loan Affordability Calculator to estimate costs tailored to you.

Final Thoughts: Your Downpayment Goal

Rules can shift with government policies, so always verify the latest with HDB, MAS, or a trusted mortgage advisor like The Loan Connection—2025 might bring surprises! Plan ahead—know your buyer category, tap grants if you can, and budget for those extras. With the right strategy, you’ll turn that homeownership dream into a confident reality.

Disclaimer:

The information provided in this blog is for general informational purposes only and does not constitute financial advice. While The Loan Connection (TLC) strives to ensure accuracy, we make no guarantees as to the completeness, reliability, or timeliness of the information. Readers are encouraged to verify details independently and consult qualified professionals before making any financial decisions. TLC is not liable for any losses or damages arising from reliance on the content herein.